Key takeaways

A donor-advised fund (DAF) is a pool of money that a nonprofit organization manages on behalf of donors.

DAFs offer both flexibility and tax benefits, including no tax on capital gains and a tax deduction in the year you make the contribution.

Donor-advised funds allow you to donate money now and recommend which charities will receive grants from your portion of the fund.

Charitable giving is a key component of a comprehensive wealth strategy for many affluent families and individuals. Creating a charitable giving plan helps you support your favorite charities while also realizing potentially valuable financial and tax benefits.

You can fulfill your charitable intentions in a variety of ways, including a donor-advised fund (DAF).

What is a donor-advised fund?

A donor-advised fund is a pool of money that a nonprofit organization manages on behalf of donors. Think of it as an investment account whose funds are used solely to support charitable organizations.

Donor-advised fund tax benefits are one of the reasons DAFs have exploded in popularity, growing from $19.66 billion in contributions in 20141 to $59.43 billion in 20232 – an increase of 202% in just under a decade.

“When you contribute highly appreciated assets to donor-advised funds, you don’t have to recognize and pay taxes on the capital gains,” says Michael Davis, senior philanthropic advisor with U.S. Bank. “You also receive an immediate tax deduction in the year when the contribution is made.”

Donor-advised funds offer flexibility

Another advantage of DAFs is their flexibility: You can donate money now and recommend later which charities will receive grants from your portion of the fund, as well as when charities receive the assets and how your contributions will be invested for tax-free growth. The charities take care of fund setup in exchange for an annual administrative fee that donors pay.

“When you contribute highly appreciated assets to donor-advised funds, you don’t have to recognize and pay taxes on the capital gains.”

Michael Davis, senior philanthropic advisor, U.S. Bank

“Donor-advised funds offer a lot of flexibility for wealthy families who are philanthropic and want to support different charitable organizations,” says Davis. “For example, maybe you want to respond to a crisis or natural disaster, such as the California wildfires or hurricanes in the southeast. Or maybe you want to make a large gift to a charity that’s especially meaningful to you and your family. This is why I call DAFs the ‘multi-purpose tool’ of charitable giving.”

Donor-advised fund rules

Nonprofit organizations may have their own rules for donor-advised funds, but here are some general rules that apply to all DAFs:

- All contributions are irrevocable; donors cannot take them back. The assets belong to the charity, while the donor retains advisory privileges.

- The charity must approve any donor grant recommendations before it disburses any assets. Charities may reject recommendations if they don’t meet their standards or guidelines.

- Grants may only be disbursed to one of the estimated two million qualified 501(c)(3) organizations that are recognized as such by the IRS.3 These may include religious and service organizations, educational institutions and food banks, among others.

- Donors may not receive any personal benefit from DAF grantmaking.

- DAF grants cannot be used to purchase tickets to galas, events or auctions or to pay for items purchased or won at charity auctions.

- DAF grants cannot be made to political candidates or parties.

Donor-advised fund tax considerations

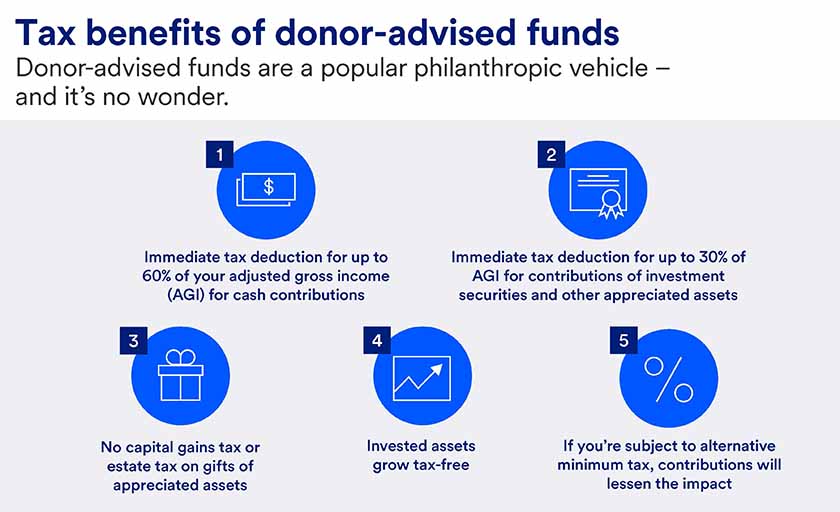

There are several donor-advised fund tax benefits you should be aware of, including:

- There’s an immediate donor-advised fund tax deduction for up to 60% of your adjusted gross income (AGI) for cash contributions and 30% of AGI for contributions of investment securities and other appreciated assets.

- No capital gains tax or estate tax is due on gifts of appreciated assets.

- Invested assets grow tax-free, which may result in additional funds to support the charity’s mission.

- Contributions may lessen the impact of the alternative minimum tax on donors.

How does a donor-advised fund work? Three high-level steps

Step 1: You make tax-deductible donations of assets to the donor-advised fund. These assets may include cash, publicly traded securities, real estate, privately held business ownership shares, cryptocurrency and tangible personal property, among others.

Step 2: Your donations grow tax-free for as long as they’re held in the fund, which makes even more money available to charities. In the meantime, you can decide which charities you’d like to support with your assets.

Step 3: You make recommendations to the fund about which charity or charities you’d like to receive grants. This way, you can support the charities you believe in at a pace that’s comfortable for you.

“By being able to make donations and recommendations on your own schedule, you can be more thoughtful and strategic with your charitable giving,” says Davis.

Donor-advised funds vs. private foundations

A private foundation is another charitable giving vehicle to consider, but what’s the difference between a donor-advised fund and a private foundation?

A private foundation is a nonprofit organization established by an individual or family that’s funded with an initial gift of assets and managed by trustees or a board of directors. Since it’s an independent legal entity, a private foundation provides more control over how donations are directed than a DAF, which only allows you to recommend which charities receive donations.

Private foundations typically require a larger initial investment than DAFs, which can be started with as little as $5,000. They also require administrative tasks such as creating a formal board of directors, holding regular meetings, making grants and filing annual tax returns. While this level of formality may be attractive for some families, it may prove to be burdensome for others.

“A private foundation is a more formal structure [than a donor-advised fund] and might be appropriate in the right situation,” says Davis. “But it’s also going to require more work and a higher level of ongoing maintenance. It requires a substantial commitment of both time and energy on the part of the family.”

Donor-advised funds: Are they right for you?

Davis recommends speaking with your wealth team for guidance on whether a donor-advised fund is the right charitable giving vehicle for you and your family.

“You should focus not just on the tax and legal implications but also on your overall charitable giving goals,” he says. “Also be sure to talk to other family members to find out what they think about philanthropy and the kinds of charities they’d like to support.”

There are many potential benefits to donor-advised funds that could make them the right charitable giving vehicle for you and your family. Speak with your attorney and other trusted advisors for help in determining if a DAF can help you meet your charitable giving goals.

Learn more about Philanthropic Services from U.S. Bank.

Explore more

The benefits of starting a private family foundation

A private foundation can help unify your family behind service-oriented causes, while developing responsibility and leadership skills that will serve the family for generations.

Bring your charitable giving vision to life.

Philanthropic Services from U.S. Bank serves individuals, families and family foundations, as well as public charities and nonprofit organizations.